Cybersecurity Insurance for Law Firms: 2026 Guide

Cybersecurity insurance for law firms is defined as a specialized policy that covers financial losses from data breaches, ransomware, and regulatory actions while simultaneously enforcing the documented security controls that ABA Model Rule 1.6(c) requires. The role of cybersecurity insurance for law firms has expanded well beyond simple financial protection. In 2026, underwriters treat the application process as a technical audit, requiring verified evidence of multi-factor authentication (MFA), endpoint detection and response (EDR), and tested offline backups before issuing coverage. Law firms face over 1,000 cyberattacks weekly, yet only 40% carry cyber insurance despite an average data breach cost of $5.08 million. That gap between exposure and protection is the defining risk management problem for every firm partner reading this.

What does cyber insurance for law firms actually cover?

Cyber insurance for law firms is not a single product. It is a bundle of coverage components, each addressing a distinct category of loss that legal practices face after a breach.

The core components found in most policies include:

- Network security liability: Covers third-party claims arising from a breach of client data stored on firm systems. For law firms holding privileged communications, merger documents, and litigation strategy, this is the most financially significant coverage layer.

- Privacy liability: Addresses regulatory fines and client notification costs when personally identifiable information is exposed. State bar investigations triggered by a breach fall under this category.

- Business interruption: Replaces lost revenue when firm systems are offline. Business interruption waiting periods typically range from 12 to 24 hours but can be negotiated down to 6 to 8 hours for ransomware events. That negotiation matters because a single day of downtime at a mid-size firm can represent tens of thousands of dollars in unbillable hours.

- Ransomware and cyber extortion: Covers ransom payments, negotiation fees, and decryption costs. Note that some state and federal regulations restrict ransom payments to sanctioned entities, so policy language must be reviewed carefully.

- Regulatory defense and bar complaints: Covers legal defense costs when a breach triggers a state bar investigation or regulatory action. This coverage is unique to professional services policies and is frequently undervalued by firm partners.

- Media liability: Addresses claims arising from inadvertent publication of confidential information online.

The table below maps each coverage component to the specific law firm risk it addresses:

| Coverage Component | Primary Law Firm Risk Addressed |

|---|---|

| Network security liability | Breached client files, privileged communications |

| Privacy liability | State bar complaints, client notification costs |

| Business interruption | Lost billable hours during system downtime |

| Ransomware/cyber extortion | Encrypted case management systems |

| Regulatory defense | Bar investigations, state attorney general actions |

| Media liability | Inadvertent disclosure of confidential client data |

Policy coverage components are well-documented, but coverage gaps are where firms get hurt. Wire fraud and social engineering losses are frequently excluded or subject to sublimits. Understanding what your policy does not cover is as important as knowing what it does.

How do underwriting requirements enforce security controls?

The insurance application process now functions as a de facto cybersecurity audit, and that shift has direct consequences for how law firms manage their IT programs.

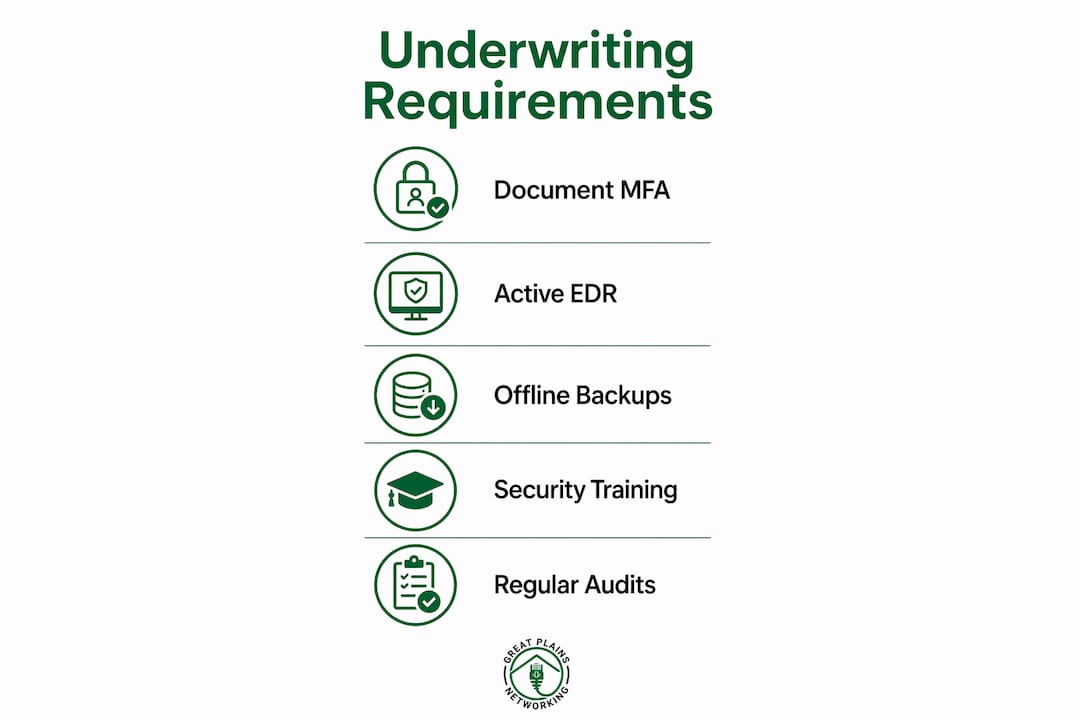

Underwriters in 2026 require granular, documented evidence of security controls. Checking a box on an application is no longer sufficient. Firms must provide proof that controls are active, tested, and applied across all systems, including remote access points and third-party vendor connections. Most cyber insurance applications now demand this level of technical evidence rather than simple attestations.

The specific controls underwriters require most consistently are:

- Multi-factor authentication (MFA): Required on all email accounts, remote desktop access, and cloud applications. Partial MFA deployment, such as applying it only to email but not to case management software, is treated as non-compliance.

- Endpoint detection and response (EDR): Active EDR software must be deployed on every device that accesses firm data, including attorney laptops and mobile devices used for client communication.

- Immutable, offline backups: Backups must be stored in a location that ransomware cannot reach and must be tested quarterly with documented restore results. An untested backup is treated the same as no backup.

- Security awareness training: Documented phishing simulation results and training completion records are increasingly required as part of the application.

- Incident response plan: A written, tested plan that identifies roles, escalation paths, and notification procedures is now a standard underwriting requirement.

Firms that cannot document these controls face premiums 2 to 5 times higher than compliant peers, or outright policy denials. That premium differential alone justifies the cost of implementing proper controls before applying for coverage.

Pro Tip: Before submitting your cyber insurance application, have your IT provider run a gap analysis against the underwriter's control checklist. Addressing deficiencies before the application avoids premium penalties and strengthens your ABA Model Rule 1.6(c) compliance posture at the same time.

The overlap between insurer requirements and ABA Model Rule 1.6(c) is not coincidental. Both frameworks require reasonable, documented efforts to protect client data. Satisfying one largely satisfies the other, which means your insurance application doubles as an ethics compliance exercise.

What exclusions and pitfalls should law firms anticipate?

Coverage denials are more common than most firm partners realize, and they almost always trace back to one of three problems: incomplete documentation, policy exclusions, or controls that were not active at the time of the breach.

The most frequent pitfalls include:

- Social engineering sublimits: Many policies cap social engineering and wire fraud losses at $250,000, far below the actual loss in a business email compromise attack. A firm wiring $800,000 based on a spoofed client email may recover only a fraction of that loss.

- Voluntary transfer exclusions: The voluntary transfer exclusion means that if a firm employee willingly transferred funds based on fraudulent instructions, the loss may not be covered under the standard cyber policy. Firms should implement and document wire verification protocols, such as callback confirmation to a known number, to reduce both the risk and the coverage dispute.

- Documentation failures at claim time: Claims are denied when the firm cannot prove that MFA or backups were active and properly configured at the time of the breach. Attestations made during the application that do not reflect actual practice expose the firm to both denial and potential fraud liability.

- Ransomware payment restrictions: Policy language may restrict payments to entities on OFAC sanction lists. If the ransomware group is sanctioned, paying the ransom could violate federal law regardless of what the policy says.

- The cyber versus legal malpractice boundary: A breach that results in a missed filing deadline may generate a legal malpractice claim, not a cyber claim. Understanding which policy responds to which loss requires careful review with a broker who specializes in legal professional liability.

Pro Tip: Negotiate your business interruption waiting period at policy renewal. Reducing it from 24 hours to 6 to 8 hours for ransomware events can protect significant revenue for a firm that bills by the hour.

How does cyber insurance improve cybersecurity posture and compliance?

Cyber insurance has shifted from a financial buffer to an operational mandate that actively drives better security practices inside law firms. The mechanism is straightforward: insurers will not cover firms that do not meet documented control standards, so firms that want coverage must build and maintain those controls.

The benefits extend beyond the policy itself:

- Pre-incident risk management services: Many insurers provide policyholders with access to vulnerability scanning tools, phishing simulation platforms, and threat intelligence feeds at no additional cost. These services reduce the probability of a claim before one occurs.

- Incident response panels: Insurers maintain pre-vetted panels of forensic investigators, breach counsel, and public relations firms. Access to these expert teams reduces incident costs by 30 to 50% compared to firms that must source and contract these services during a crisis. That reduction is significant when the average breach costs $5.08 million.

- Premium incentives for strong programs: Firms with documented, tested security programs receive lower premiums. That financial incentive creates a direct return on investment for IT security spending that partners can present to firm leadership.

- Alignment with state bar standards: Several state bars have adopted cybersecurity guidance that mirrors ABA Model Rule 1.6(c). Insurance-driven controls satisfy both the insurer and the bar, reducing the risk of disciplinary action following a breach.

"Insurers are now functioning as de facto cybersecurity regulators for law firms. Their underwriting requirements set a practical floor for security standards that ethical rules alone have not enforced consistently."

The synergy between insurance requirements and law firm cybersecurity controls means that firms investing in MFA, EDR, and tested backups are simultaneously reducing their premium costs, satisfying ABA obligations, and lowering their actual breach risk. These are not separate programs. They are the same program viewed from three different angles.

Key takeaways

Cybersecurity insurance for law firms is both a financial instrument and a compliance enforcement mechanism that requires documented, tested security controls to function effectively.

| Point | Details |

|---|---|

| Coverage is multi-layered | Policies cover network liability, business interruption, ransomware, and regulatory defense as distinct components. |

| Underwriting is a security audit | Insurers require documented MFA, EDR, and tested backups; non-compliance triggers premiums 2 to 5 times higher. |

| Exclusions create real gaps | Social engineering sublimits and voluntary transfer exclusions limit recovery in common wire fraud scenarios. |

| Insurance drives compliance | ABA Model Rule 1.6(c) controls and insurer requirements overlap significantly, satisfying both with one program. |

| Incident response panels reduce costs | Pre-vetted insurer response teams reduce breach costs by 30 to 50% compared to uninsured firms. |

Why partners cannot afford to delegate this decision

Most firm partners treat cyber insurance as an administrative task and hand it to office managers or IT staff to complete. That approach creates serious exposure. Inaccurate attestations on an insurance application expose the signing partner to personal liability and can void coverage at the worst possible moment.

I have seen firms complete detailed insurance applications that bore no resemblance to their actual IT environment. MFA was checked as "fully deployed" when it covered only email. Backups were listed as "tested quarterly" when no restore test had been performed in over a year. When a breach occurred, the insurer denied the claim based on material misrepresentation. The firm faced the full $5 million breach cost without coverage.

The insurance application is not a formality. It is a legal document that a partner must personally review against the firm's actual technical controls. That requires a working relationship with your IT provider, not just a signature on a form someone else prepared.

Routine security audits aligned to both insurance requirements and ABA Model Rule 1.6(c) are the most practical way to keep attestations accurate. Selecting a broker who specializes in legal professional liability, rather than a generalist commercial broker, makes a measurable difference in policy terms and claim outcomes. The same applies to your IT provider. A managed IT firm with experience in law firm IT support understands the specific documentation standards that underwriters and bar associations require.

Proactive policy reviews at each renewal cycle, not just at inception, catch exclusions that have been added or sublimits that no longer reflect your firm's risk profile. Cyber insurance is not a set-and-forget purchase.

— Nicholas

How Greatplainsnetworking supports law firms' insurance and compliance needs

Law firms in Norman, Moore, and Oklahoma City face the same underwriting requirements and ABA obligations as firms in any major market. Meeting those requirements demands documented, verified controls, not just good intentions.

Greatplainsnetworking implements and documents MFA, EDR, and immutable offline backups specifically to satisfy cyber insurance underwriting standards and ABA Model Rule 1.6(c) requirements. The firm's managed IT support includes 24/7 monitoring, quarterly backup testing with documented restore results, and incident response coordination. Proactive security training reduces phishing risk and supports the documentation insurers require at renewal. For law firms that need to close the gap between their current IT posture and what underwriters demand, Greatplainsnetworking provides the verified, documented controls that protect coverage and reduce premiums. Explore cybersecurity services built for legal practices.

FAQ

What does cyber insurance cover for law firms?

Cyber insurance for law firms covers network security liability, privacy liability, business interruption, ransomware payments, regulatory defense costs, and media liability. Each component addresses a distinct category of loss that legal practices face after a breach.

How much does cyber insurance cost for lawyers?

The cost of cyber insurance for lawyers varies based on firm size, revenue, and documented security controls. Firms lacking MFA, EDR, or tested backups face premiums 2 to 5 times higher than compliant peers, making security investment a direct cost control measure.

What security controls do insurers require from law firms?

Underwriters require documented MFA on all systems, active EDR on every device, quarterly tested offline backups, security awareness training records, and a written incident response plan. Partial deployment of any control is treated as non-compliance.

Can a cyber insurance claim be denied after a breach?

Yes. Claims are frequently denied when firms cannot prove that required controls were active and properly configured at the time of the breach, or when losses fall under voluntary transfer or social engineering exclusions.

How does cyber insurance relate to ABA Model Rule 1.6(c)?

ABA Model Rule 1.6(c) requires reasonable efforts to protect client information. The controls insurers mandate, including MFA, EDR, and tested backups, satisfy this ethical standard, meaning a compliant insurance program and bar compliance are effectively the same program.

Recommended

Want help putting this into practice?

We'll audit your security, speed, and hardware in under an hour — no commitment, no sales pitch. Just a clear roadmap of what to fix and why.